Seismic changes are taking place in Europe. Prompted by signs that the

traditional U.S. security support could be withdrawn or at least

downsized, the German parliament recently passed landmark fiscal stimulus

measures, a move which had eluded generations of lawmakers. The country is

now poised to enter a new phase, in our view, moving beyond a period in

which fiscal constraints stifled growth and undermined competitiveness.

The German fiscal package relaxes the limitation on structural deficits to

allow for higher defense spending, a measure that effectively leaves

defense spending unconstrained. It also creates a special fund for

infrastructure investments of as much as €500 billion (or a sizeable

12 percent of annual GDP) over the next 12 years. Transport, hospitals and

care, energy, education, digitization, and R&D are all targeted.

It is notable that these measures were championed by chancellor-to-be

Friedrich Merz, leader of the CDU/CSU party, who had recently campaigned

on preserving fiscal restraint. His significant pivot points to the

seriousness of both the situation and the commitment.

Meanwhile, the European Commission has proposed a plan to address

deficiencies in the region’s defense capabilities by 2030, with

recommended funding of up to €800 billion. This includes €150 billion of

joint EU loans for defense investment and making defense spending by

member states exempt from the bloc’s deficit rules.

Joint debt issuance has long been a contentious issue within the EU, and

historically has been reserved for times of crisis such as the COVID-19

pandemic. Wealthier northern member states have been reluctant to

subsidize their less-affluent neighbors, making such measures politically

sensitive. The fact that joint issuance is once again being considered

underscores the urgency of the current situation and suggests willingness

to strengthen financial unity within the bloc may be growing. European

Union leaders will now seek approval for the plan in their own countries.

Improving economic prospects

These changes are occurring as the region’s domestic economy is picking

up. RBC Capital Markets economists point out that real incomes have grown

modestly as inflation has subsided. This and the delayed pass-through of

the European Central Bank’s (ECB) cuts to outstanding mortgage rates

should underpin a revival of consumption.

Economic activity indicators such as the HCOB Eurozone Composite

Purchasing Managers’ Index are now narrowly in expansion territory.

The underlying European economy is running above long-term average growth

rates

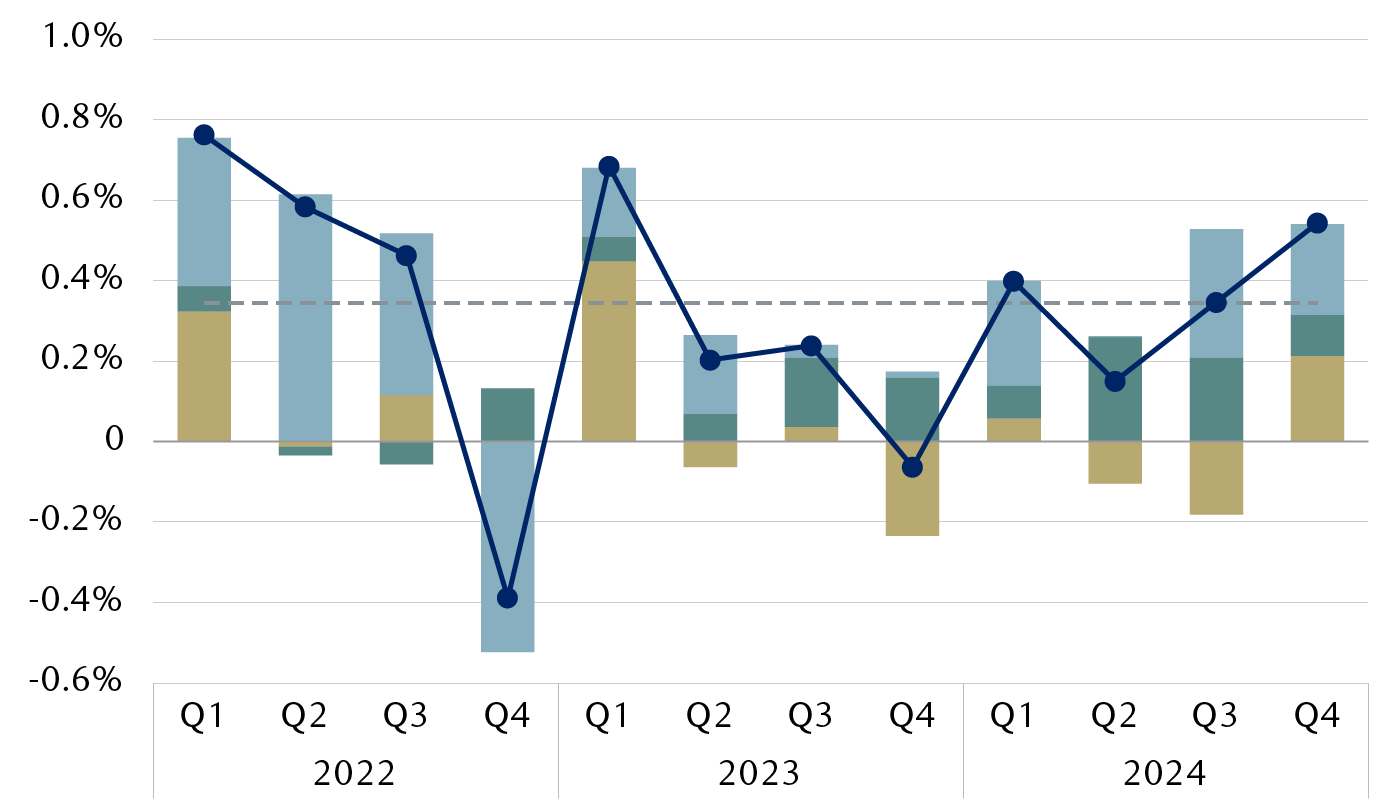

Contributors to European Union GDP growth

The graph shows a quarterly breakdown of European Union GDP since Q1

2022 and three major contributors to it: private consumption,

government consumption, and fixed investment. The data has been very

volatile over this period. Private consumption played a very modest

role from Q2 2023 to Q2 2024. Since Q3 2024, it has become a more

important driver of economic growth. In Q4 2024, all three

contributors had a positive impact on growth and since Q2 2024, the

economy has grown consistently quarter over quarter.

-

Private consumption

-

Government consumption

-

Fixed investment

-

Final domestic demand q/q

-

Long-term average demand

Note: Ireland excluded due to volatile data.

Source – RBC Wealth Management, RBC Capital Markets, Haver Analytics,

Eurostat

Germany’s fiscal package and the EU’s defense spending are also modest

tailwinds. RBC Capital Markets economists calculate that Germany’s

infrastructure spending, if ramped up over the next three years, could have a

growth impact of 0.5 percent of GDP per year for the country, or

0.15 percent for the euro area. The impact could be larger in the near

term if spending is front-loaded. Moreover, they estimate that increasing

the EU’s overall defense spending to three percent of GDP in 2030 from the

current 1.4 percent could have a direct impact of 0.3 percent per year on

real GDP growth, on average, by 2030. However, they concede that this is

an aggressive assumption, given that most Western militaries are already

suffering recruitment challenges even before any additional spending.

RBC Capital Markets recently increased its overall eurozone GDP growth

projections by approximately 0.5 percentage points per year, bringing

anticipated GDP growth to 1.9 percent in 2026 and 1.8 percent in 2027.

Tariff uncertainty continues

The clear risk to these estimates is a trade war. RBC Global Asset

Management Inc. Chief Economist Eric Lascelles maintains that the impact

of tariffs on European economies is “unlikely to be too painful,” because

unlike Canada and Mexico, Europe does not trade intensively enough with

the U.S. The ECB had calculated that a 25 percent blanket tariff could

crimp regional GDP growth by 0.3 percentage points over 12 months. Though

the tariffs imposed by the White House are a little lower, at 20 percent,

the impact on economic growth will depend on how long they are sustained,

how the EU responds, and how badly the new trade policies hurt business

and consumer confidence both in the region and globally.

Lascelles continues to believe that a deal will be struck eventually, and

that lower, partial tariffs will end up being imposed, much like during

the first Trump presidency—though this could take many months. In the

meantime, the economies of the largest European exporters to the U.S.

(including Germany and Italy) are likely to bear the brunt of impacts. The

effect on corporate earnings should be relatively limited given that many

companies have manufacturing operations in the U.S.

For now, we believe the new positive fiscal impulse in the euro area

should offset the negative tariff impact, though we acknowledge the risk

to growth may well be downwards.

Planning a new itinerary

The European Union’s structural issues, including a lack of investment by

Germany, have been a key reason for global investors’ caution towards the

European stock market. Recent developments suggest the bloc may be ready

to tackle those issues, acting with urgency and cohesion. Reflecting this

sentiment, markets have rallied year to date—but unbridled enthusiasm has

given way to skepticism about implementation. Very large stimulus programs

come with risks, including timing challenges and the potential for

misallocation of funds. Tariff worries are also weighing on regional

equities.

Nevertheless, we believe that on a 6-to-12-month horizon, a Market Weight

position in the region is now appropriate, up from an Underweight. This

new positioning better reflects the improved outlook, while acknowledging

that U.S. tariff developments could lead to volatility.

European equity valuations remain close to an all-time low relative to

U.S. and global peers on a sector-adjusted basis. In our view, being

selective and taking an active approach are crucial for this region, as it

provides a rich and varied opportunity set for stock selection. We believe

there are potential opportunities in Europe’s world-leading companies with

structural global tailwinds, particularly in Technology, Health Care, and

Industrials. We also see opportunities in niches exposed to the improving

domestic picture and to areas targeted by new fiscal policies, including

banks, defense, and capital goods.

With contributions from Thomas McGarrity, CFA

RBC Wealth Management, a division of RBC Capital Markets, LLC, registered investment adviser and Member NYSE/FINRA/SIPC.

Managing Director, Head of Investment Strategy

RBC Europe Limited

link