June 18, 2025

Alan Robinson

Vice President

Global Portfolio Manager

Key points

-

Tariff upheaval has triggered a renewed interest in global equity

diversification as a hedge against volatility in individual markets. -

This comes as the trade-weighted Dollar Index is under pressure due to

concerns over the sustainability of U.S. fiscal deficits. -

While we don’t think the age of “U.S. exceptionalism” is over, we do

think the recent dramatic shifts in U.S. policy provide a catalyst to

reassess geographic exposures in a global portfolio.

Tariff upheaval triggers a rally in overseas stocks

The first five months of 2025 have seen a seismic shift in global trade

norms as U.S. President Donald Trump seeks to use tariff threats as a tool

to achieve his policy goals on the international stage, and as a way to

raise revenue.

The initial new tariff schedule announced on April 2 effectively raised

the average tariff charged by the U.S. to 19 percent from three percent,

with wide variations across trading partners. The most punitive tariffs

are on hold pending trade negotiations, and we believe the complexity of

inking lasting trade deals suggests that many of these tariffs will

quietly go away. But the uncertainty generated by shifting trade rules is

likely to impact investment patterns globally over the long term.

The U.S. economy is the most self-contained of all the world’s developed

economies. On the surface, this suggests new policies that stymie trade

should impact the U.S. less than its trading partners; however, the tariff

upheaval has revealed how deeply integrated U.S. companies are in the

global economy and supply chains.

While all global trading blocs now face higher tariffs, during the first

100 days of Trump’s second term, investors in European stocks have fared

better than those investing in U.S. stocks. This is atypical for new

administrations and is different from Trump’s first term, which had more

in common with those of the presidents who bookended it, at least in terms

of relative equity performance.

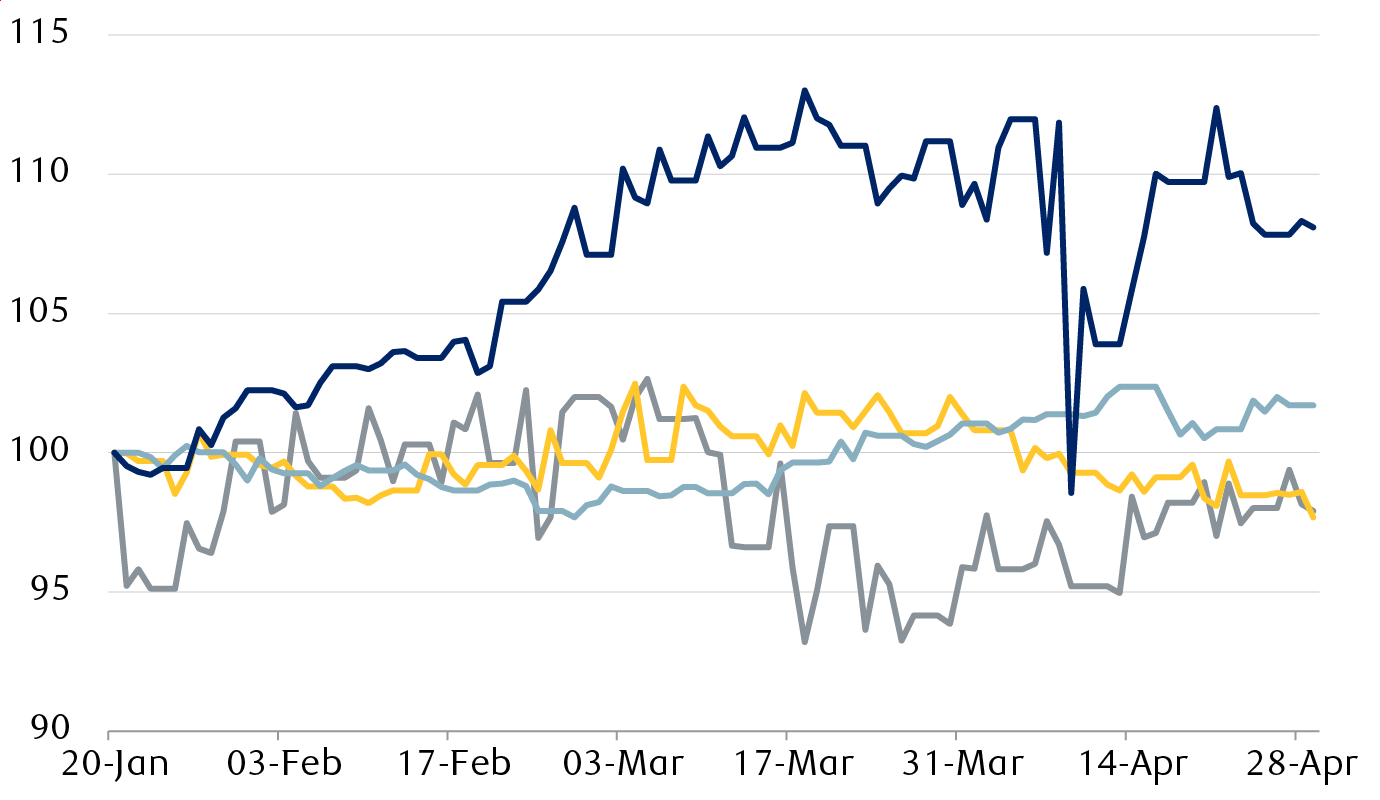

New administration policies have favored European stocks

STOXX Europe 600 vs. S&P 500 in first 100 days of presidential terms

This line chart shows the performance of the STOXX Europe 600 Index

relative to the S&P 500 Index for the first 100 days of the four most

recent presidential administrations. During the initial stages of the

Obama and Biden administrations in 2009 and 2021, European stocks

underperformed U.S. stocks by 2% over the first 100 days. European

stocks outperformed by 2% in the initial stages of Trump’s first term

in 2017, and by 8% in Trump’s second term in 2025.

-

Obama (2009)

-

Trump 1 (2017)

-

Biden (2021)

-

Trump 2 (2025)

Source – RBC Wealth Management, FactSet; daily index data in local

currency, normalized, with first day of term = 100

Why did international stocks outperform?

One of the common narratives from market pundits analyzing this period of

international stock outperformance concerned “the end of U.S.

exceptionalism.” This posited that no economy would emerge unscathed from

the trade upheaval and that the global stability and low prices that had

fueled U.S. consumer spending and driven outsized U.S. corporate profit

growth were at an end. This was accompanied by concerns that the

reliability of U.S. institutions and legal norms was at risk.

We would push back against this narrative. While some overseas

institutions repatriated securities held in the U.S., there was no

wholesale flight, in our view. Instead, the new, more uncertain paradigm

encouraged investors to rebalance portfolios that had long been overweight

U.S. stocks as “the only game in town.” The tariff upheaval was the

catalyst to put money to work in foreign equities that had long traded at

a significant discount to U.S. stocks.

The tariff storm shook the governments of several of the U.S.’s trading

partners out of their policy complacency. Many countries turned to their

fiscal stimulus playbook, further helping sentiment toward international

stocks. Germany, in particular, abandoned its long-held fiscal deficit

limit to invest heavily in defense and infrastructure.

There was a clear pattern of outperformance by overseas stock markets,

based on the extent of fiscal and monetary stimulus, with the more

cautious Japanese government pouring cold water on the hopes of a looser

monetary policy, which limited the gains in Japanese stocks.

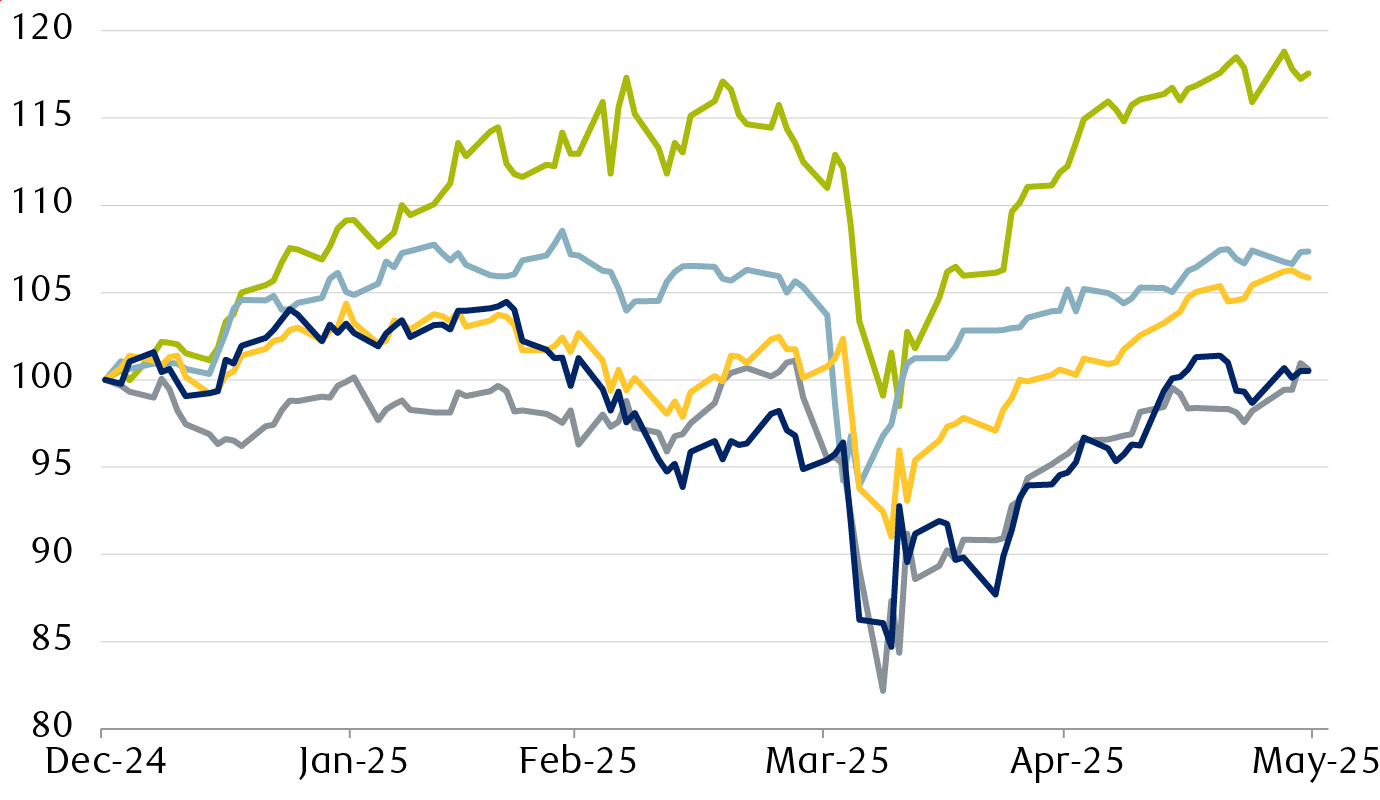

International equities have produced broad-based gains versus the U.S.

Relative performance of developed-market equity indexes

This line chart shows the relative performance of the major stock

market indexes of Germany, the UK, Canada, Japan, and the U.S. for the

first five months of 2025. Germany, the UK and Canada outperformed

during the year, with price gains of 18%, 7% and 6% respectively.

Japan and the U.S. ended the period roughly flat on the year.

-

Germany (DAX)

-

Canada (S&P/TSX)

-

UK (FTSE 100)

-

Japan (TOPIX)

-

U.S. (S&P 500)

Source – RBC Wealth Management, FactSet; daily data through 5/30/25,

normalized with 12/31/24 = 100

The weaker dollar boosts foreign currency assets further

While foreign investors celebrated gains in their domestic stock markets,

U.S.-based investors with overseas exposure did even better relative to

their home market. This was because the value of the dollar declined

against major currencies, and this inflated the value of overseas stocks

denominated in appreciating foreign currencies.

For example, the German DAX Index gained 17 percent over the five months

ending May 2025, while the S&P 500 Index eked out a one percent gain.

But the 10 percent gain in the value of the euro against the dollar over

that period served to almost double the return of the German equity

market, from the perspective of dollar-based investors, with UK and

Japanese stocks enjoying a similar tailwind to dollar-denominated returns.

International stock returns have been even better in U.S. dollar terms

2025 year-to-date equity market returns

This bar chart shows the stock market returns of the U.S., Germany,

France, the UK and Japan for the first five months of 2025 in local

currency terms and in U.S. dollar-denominated terms. The U.S. market

gained approximately 1%, while Germany gained 18%, France 5%, the UK

7%, and Japan 1%. However, in dollar terms Germany gained 30%, France

17%, the UK 16%, and Japan 11%.

-

In local currency

-

In U.S. dollar terms

Source – RBC Wealth Management, FactSet; data through 5/30/25

Part of the decline in the value of the dollar was attributed to

statements from Trump suggesting he’d be happy with a declining dollar, as

this would make U.S. exports more competitive.

Some of these statements were walked back by his cabinet, but the global

rebalancing discussed above, together with a historically overvalued

dollar leading into Trump’s second term, kept pressure on the greenback.

This period of dollar weakness stands in contrast to the relative

stability of the currency during the first few months of previous

administrations.

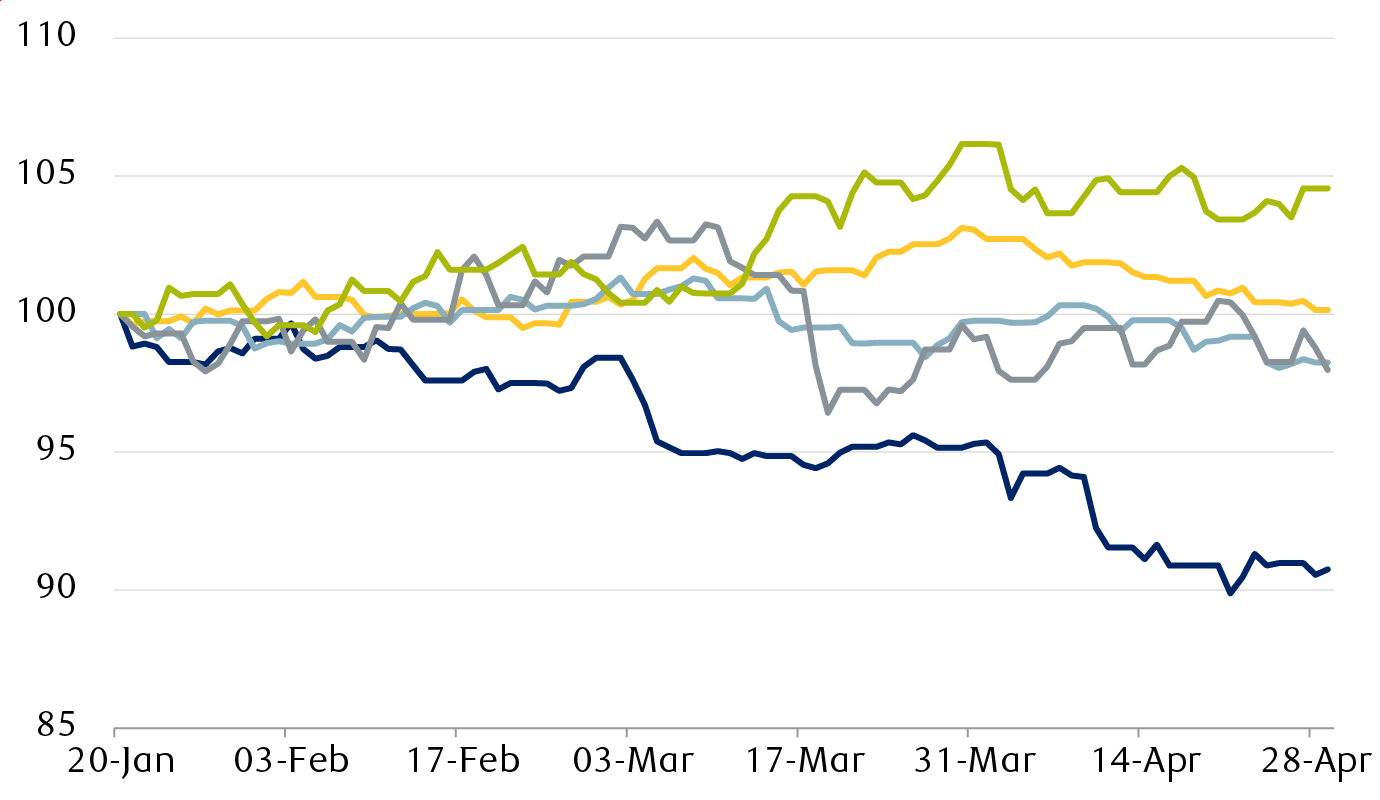

Trade rhetoric pressures the U.S. dollar

U.S. dollar performance in first 100 days of presidential terms

This line chart shows the performance of the trade-weighted U.S.

Dollar Index (DXY) for the first 100 days of the five most recent

presidential administrations. During the initial stages of the Biden

(2021) and G.W. Bush (2001) administrations, the dollar rallied

slightly against major currencies. The first 100 days of the Obama and

first Trump administrations in 2009 and 2017 saw slight declines in

the dollar of around 2%. Over the first 100 days of Trump’s second

term, the dollar declined by 9%.

-

Trump 2 (2025)

-

Biden (2021)

-

Trump 1 (2017)

-

Obama (2009)

-

G.W. Bush (2001)

Source – RBC Wealth Management, FactSet; daily data, normalized with

first day of term = 100

The weakness of the dollar so far in 2025, while significant, pales in

comparison to the currency’s gains since its cycle low in 2008. The

trade-weighted U.S. Dollar Index, or DXY, gained 62 percent from March

2008 to its peak in 2022. The nine percent decline in the DXY over the

first five months of 2025 has put a dent in that, but the currency is

still overvalued on a purchasing power parity basis by as much as 12

percent against the euro, 14 percent against the Canadian dollar, and a

whopping 70 percent against the Japanese yen as of the end of Q1 2025.

The dollar’s multiyear bull trend is looking long in the tooth

U.S. Dollar Index (DXY)

This line chart shows the performance of the trade weighted U.S.

Dollar Index (DXY) over the last 30 years. From 1995 to 2002, the DXY

increased from 80 to 120. It then declined to 72 by 2008 before

peaking at 111 in 2022. Since then, the DXY has declined to 99.

Source – RBC Wealth Management, FactSet; data through 5/30/25

From our vantage point, if the dollar starts on a new bear cycle, overseas

assets will start to look more appealing for U.S. investors. And investors

outside of the U.S. will no longer have the benefit of a strong dollar

acting as a tailwind to the returns of their U.S. assets. This will likely

result in further rebalancing away from the U.S. as the dollar declines,

and foreign investors’ sales of U.S. assets will weaken the dollar further

in a gradual feedback loop.

Changes in export patterns caused by higher tariffs will further

complicate the issue, in our opinion. If overseas exporters sell fewer

goods into the U.S., they will receive fewer dollars in return from U.S.

consumers and businesses. These dollars would have likely been invested

back into U.S. stocks and bonds, so a decline in trade may reduce the fuel

needed to support U.S. asset markets.

No reason for U.S. investors to stray from home base … until now?

The rally in international stocks relative to their U.S. peers this year

has gained a lot of attention. But their recent outperformance is eclipsed

by the consistent outperformance of U.S. stocks since 2010. Over that time

frame, U.S. stocks’ annual returns beat those of their peers in 13 of the

15 years through 2024, and using a five-year rolling return metric favored

by long-term investors, the U.S. has outperformed consistently over that

period.

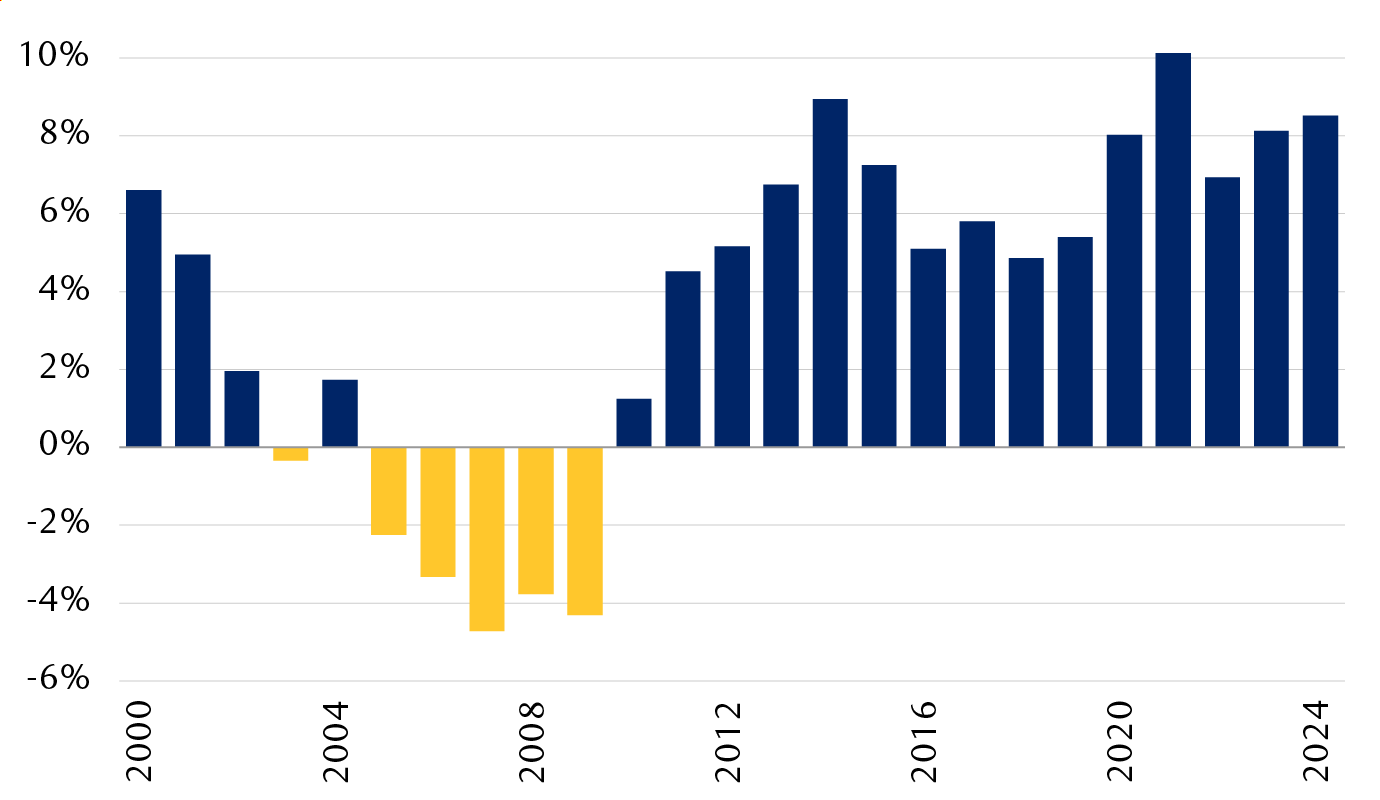

Will U.S. stocks ever stumble?

Annualized performance difference of five-year rolling returns

This bar chart shows the difference in 5-year rolling returns between

the S&P 500 Index and the MSCI All Country World ex USA Index for each

year since 1999. The S&P 500 has outperformed consistently by 5% to

10% each year since 2010, following five years of consistent

outperformance by non-U.S. stocks.

-

U.S. outperforms

-

Rest of world outperforms

U.S. stocks represented by the S&P 500 Index, rest of world by the

MSCI All Country World ex USA Index.

Source – RBC Wealth Management, FactSet

Most of this historical outperformance has coincided with the dollar bull

market discussed above. If the dollar cycle switches to a bear market

similar to the 1999–2009 period, we believe international investors’

appetite for non-U.S. stocks will resurface, as the MSCI All Country World

Index beat the S&P 500 in seven out of those 11 years.

U.S. exceptionalism under the microscope

There are usually wide disparities between the composition of equity

markets of different nations. Larger economies tend to have larger stock

markets, when measured by market capitalization. But the relationship is

not linear, with the U.S. as an extreme outlier. In fact, the U.S. economy

accounts for about 20 percent of the total global economy, but the U.S.

stock market represents 65 percent of global stock market capitalization.

Why is there such an apparent discrepancy? One element is the relative

valuation of stocks. U.S. stocks typically trade at higher

price-to-earnings (P/E) valuations than their developed-market peers for

well-understood reasons.

One is the composition of stocks across different sectors. The U.S. has a

higher proportion of technology stocks than other countries. Technology

companies tend to grow revenues and profits more quickly than companies in

other sectors, so their stocks are afforded a higher valuation. The U.S.

also has a lower proportion of Materials sector and commodity stocks

relative to other developed markets. This can be a drag on the U.S.

market’s relative performance when value-themed stocks outperform, given

these stocks are over-represented in these sectors. But their scarcity in

the U.S. indexes adds to the average valuation multiple.

Another reason is the regulatory and taxation environment, which tends to

be more friendly to companies in the U.S. The more relaxed regulatory

environment allows U.S. companies to be more nimble when cutting costs due

to slowing growth. In contrast, non-U.S. companies tend to have higher

fixed costs that provide more operating leverage when economic growth

accelerates.

A third relates to the well-established legal and oversight systems in the

U.S. that typically provide more disclosures and visibility into a

company’s business, and by implication less relative risk. And, of course,

the U.S. dollar’s reserve currency status also supports higher valuations

and deeper asset markets as international investors need somewhere to park

their dollars.

So, there are clear reasons to support a valuation premium in U.S. stocks

relative to overseas markets, but we would argue that the pendulum may

have swung too far, particularly if the previously stable taxation and

regulatory environment becomes more uncertain. While the P/E difference

between U.S. and European stocks has typically ranged between one to four

points over the last bull cycle, the difference at the end of 2024 was a

startling eight points.

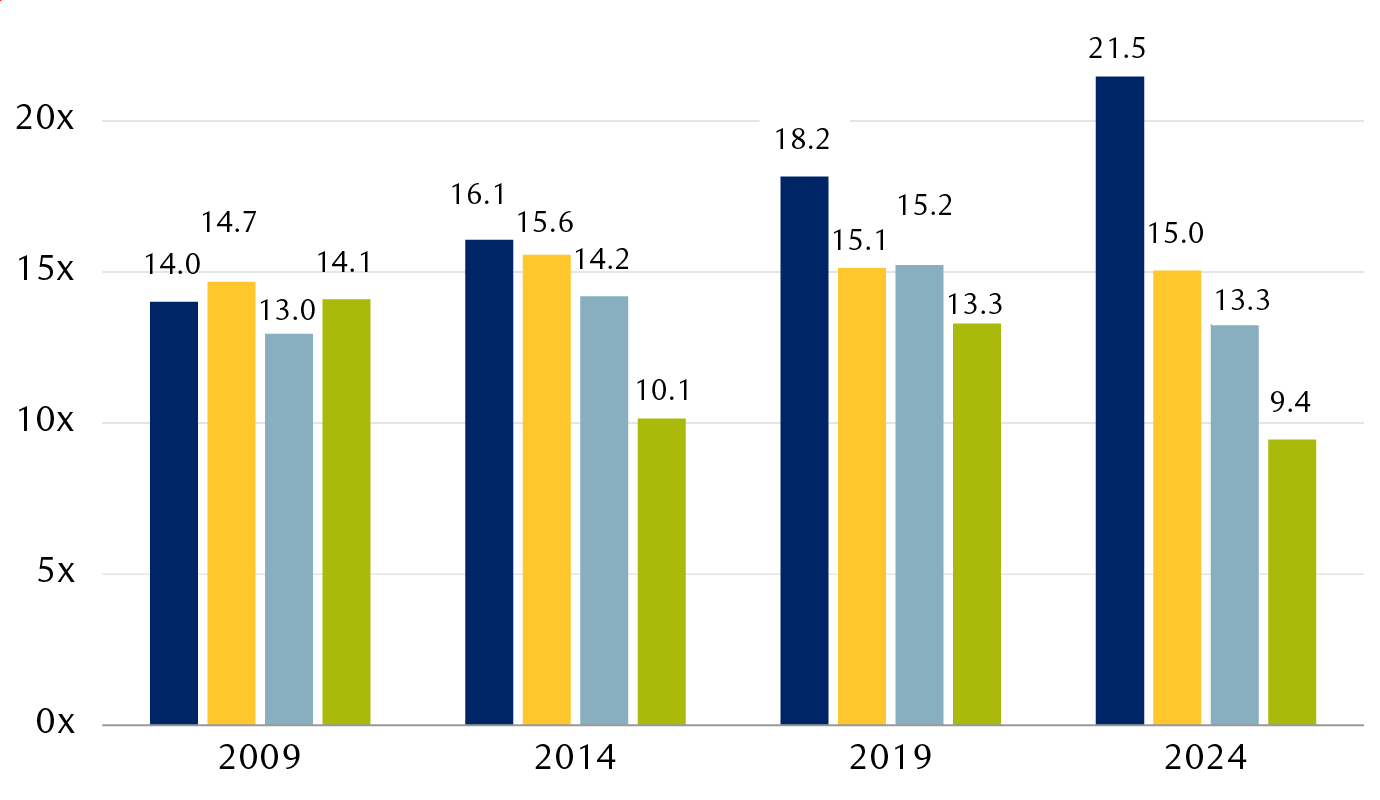

Will international investors shop around for cheaper opportunities?

Historical price/earnings (P/E) multiples

This bar chart compares the forward price/earnings (P/E) multiples of

the stock markets of the U.S., Canada, Europe, and Hong Kong in 2009,

2014, 2019 and 2024. In 2009, all four markets traded at a P/E between

13x and 15x. In the other three periods, the U.S. market traded at a

gradually increasing premium valuation to the other markets,

culminating in a 21.5x P/E in 2024 for the U.S. market versus 15x in

Canada, 13.3x in Europe, and 9.4x in Hong Kong.

-

U.S. (S&P 500)

-

Canada (S&P/TSX Composite)

-

Europe (STOXX 600)

-

Hong Kong (Hang Seng)

Source – RBC Wealth Management, FactSet; P/Es as of 5/30/25 based on

next-12-month consensus earnings estimates

Is the U.S. running low on fiscal firepower?

The Trump administration’s push to renew the tax cuts introduced in the

2017 Tax Cuts and Jobs Act, and to add significant additional tax breaks,

has refocused the market’s attention on U.S. fiscal sustainability. The

U.S. government ran a fiscal deficit of 7.7 percent in 2024 (the fiscal

deficit combines the budget deficit plus government borrowings). This was

the widest deficit of any major country and may expand further if the

proposed tax cuts eclipse any resulting economic growth.

This can be negative for U.S. assets in two ways: it can drive up interest

rates as bondholders ask for more compensation for the added risk, and it

can dampen the economic thrust that fiscal stimulus brings to bear as the

government bumps up against spending limits. And slower economic growth is

clearly a headwind for stocks.

Other countries are in a less onerous position. Many developed nations

keep their fiscal powder dry in anticipation of economic downturns, and

some have now started spending as the global economy slows, with Germany a

clear example. If other countries have more fiscal flexibility than the

U.S., their asset markets may fare better.

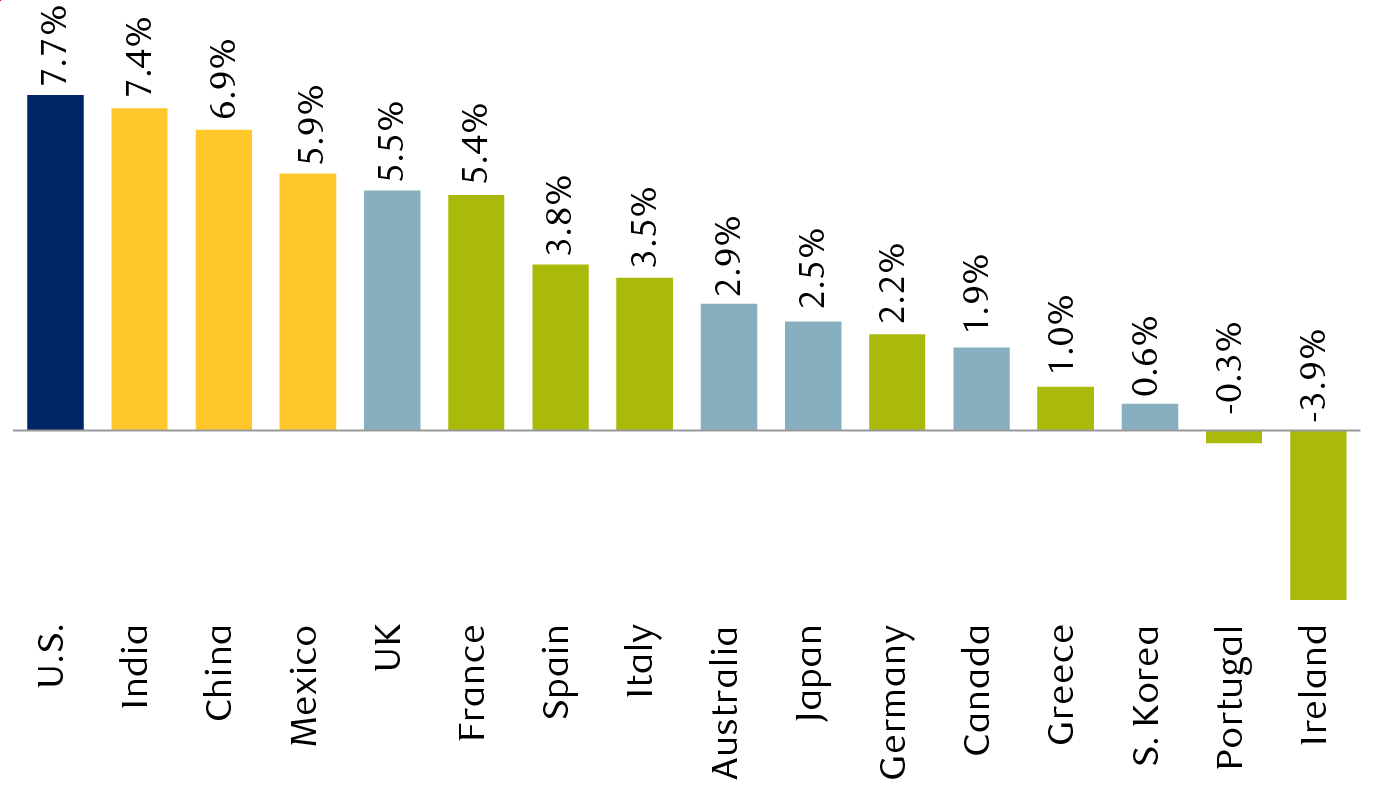

The fiscal punch bowl may start to run dry

2024 annual fiscal deficits as percentage of GDP

This bar chart shows the 2024 fiscal deficits of 16 major economies as

a percentage of each country’s GDP, ranked from largest deficit to

largest surplus. The U.S. had the largest deficit at 7.7% of GDP,

followed by India at 7.4% and China at 6.9%. Most other developed

economies had fiscal deficits between 0% and 5%, with Ireland enjoying

a fiscal surplus of 3.9%.

-

U.S.

-

Europe

-

Other developed economies

-

Emerging economies

Source – RBC Global Asset Management, RBC Wealth Management,

International Monetary Fund

An international hedge

The combination of global rebalancing and a weaker dollar has acted as a

strong tailwind for international stock performance for U.S.-based

investors through the first five months of 2025. There is evidence from

fund flow data that non-U.S. investors are pulling their assets back

closer to home, and the cracks in the geopolitical landscape caused by the

tariff changes appear to be pushing some countries closer together.

Examples include the “EU reset” that may bring the UK closer to the EU in

some economic areas after the turmoil of Brexit and vocal support for

Canada’s nationhood from the British monarchy. This lowering of economic

and geopolitical barriers outside of North America may provide new support

for overseas growth, in our opinion. And this may be supported by the

growing gulf in fiscal flexibility that overseas economies have relative

to the U.S.

On the other hand, the U.S. economy and equity markets retain significant

advantages over their international peers. Artificial intelligence

investments continue to favor U.S.-based software and technology

infrastructure companies, and the potential for an increase in U.S.

onshoring of manufacturing may provide a boost much further down the line.

Against this backdrop, we would not chase the international outperformance

seen this year, but we would also not want to be underweight international

stocks in a long-term portfolio. A balanced portfolio of high-quality

international stocks at reasonable valuations remains an important asset

allocation component for long-term investors, in our view.

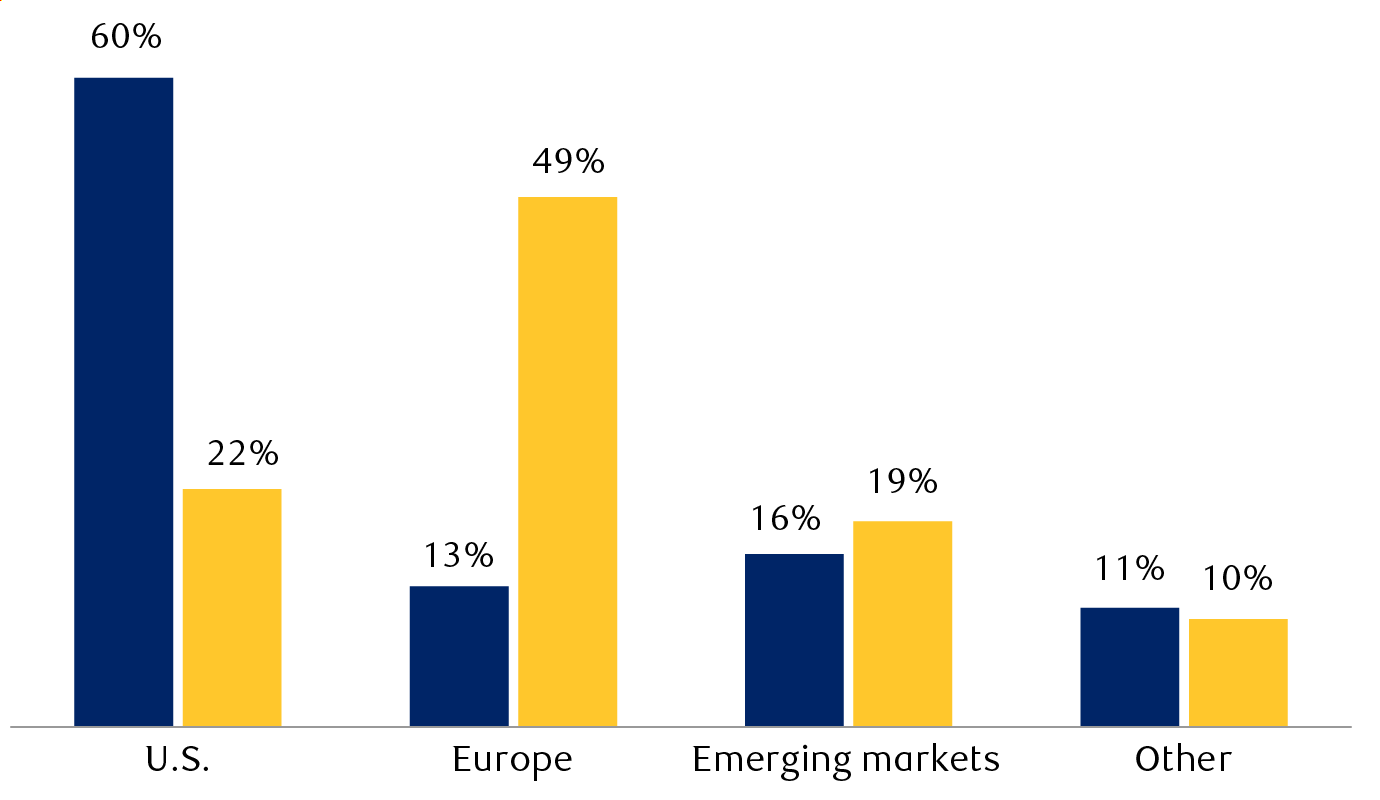

Similar businesses, different customers

U.S. and European stocks’ revenue exposure by region

This bar chart shows the aggregate geographic revenue exposure of

stocks in the S&P 500 Index and the STOXX Europe 600 Index. While the

S&P 500 draws 60% of its revenues from the U.S., the STOXX Europe 600

has only 22% exposure to U.S. customers. In contrast, the European

index draws 49% of its revenues from Europe while the S&P 500 draws

only 13% of its revenues from Europe. The remaining revenues of both

come from the rest of the world.

-

U.S. (S&P 500 Index)

-

STOXX Europe 600

Source – RBC Wealth Management, FactSet estimates for 2025

And if economic growth patterns diverge over the medium term, balanced

exposure to end markets in different parts of the world should moderate

the risk of an economic misstep in any individual market.

RBC Wealth Management, a division of RBC Capital Markets, LLC, registered investment adviser and Member NYSE/FINRA/SIPC.

Vice President

Global Portfolio Manager

link