By The Global Portfolio Advisory Committee

Quarter-century crossroads

As macro themes that endure for decades arguably matter the most to financial

markets, Eric Lascelles, chief economist at RBC Global Asset Management Inc.,

ponders what is in store for the second quarter of the century. He believes

that some long-standing themes will likely recur, some relatively new themes

may persist, and new themes may emerge.

Continuation of longstanding themes:

-

China should still be able to generate remarkable, if

somewhat slower, economic growth -

The global middle class should continue to grow, as

emerging economies rise -

Demographic challenges are set to intensify with fertility

rates continuing to drop and longevity rising -

The tech sector looks capable of remaining at the centre of

economic growth

Recent themes that may persist:

-

The relatively recent

pivot from a U.S.-led Western hegemonic world order to a

multipolar world framework wherein multiple countries play leadership roles -

The shift from a rules-based to a power-based global order,

in which stronger countries are less inclined to respect international

norms, could raise the risk of conflict and points to higher military

spending ahead -

Artificial intelligence is likely to remain a central theme

for decades -

The fading of the political will to act against climate change

may continue even as the visible effects of it, including migration from

most affected countries, become more visible -

Deglobalization will likely continue—perhaps at a somewhat

less frenetic pace than recently -

The bond market may remain more

alert to fiscal excesses, leading to a relatively steep

yield curve

Emergent themes:

-

The U.S.’s economic growth advantage could erode as

immigration declines and other public policy decisions undermine some

fraction of long-term growth. As a result, the clout of the U.S. dollar and

the Treasury market could decline somewhat over time -

Productivity should grow faster thanks to a confluence of

exciting and potentially revolutionary technologies including AI

applications in robotics and sensors, health-care innovations, and beyond -

Oil demand could peak around 2029–2034, though oil prices

will continue to be determined by the interplay between demand and supply -

India and Southeast Asian nations could become increasingly

influential

in the global economy given their large populations and rapid growth -

The stock market could generate more modest returns

given limits to how much further valuations and profit margins can rise from

current levels

Global equities: More but less

We think “positive” rather than “above average” is the outcome to plan for.

The “positive returns” outcome depends on the major economies, especially the

U.S., avoiding recession and the current consensus forecast for GDP, earnings

growth, inflation, and interest rates to be close to consensus forecasts.

The conditions necessary for the S&P 500 to deliver mid-single-digit

returns plus dividends in 2026 are likely to occur, in our view. These include

some slight further moderation in inflation allowing another cut or two from

the Fed, leaving S&P 500 earnings close to the 2026 consensus estimate of

$310 per share. Resilient business and consumer confidence, the lagged effect

of monetary easing, and tax-friendly policies should all help boost U.S. GDP

and earnings growth.

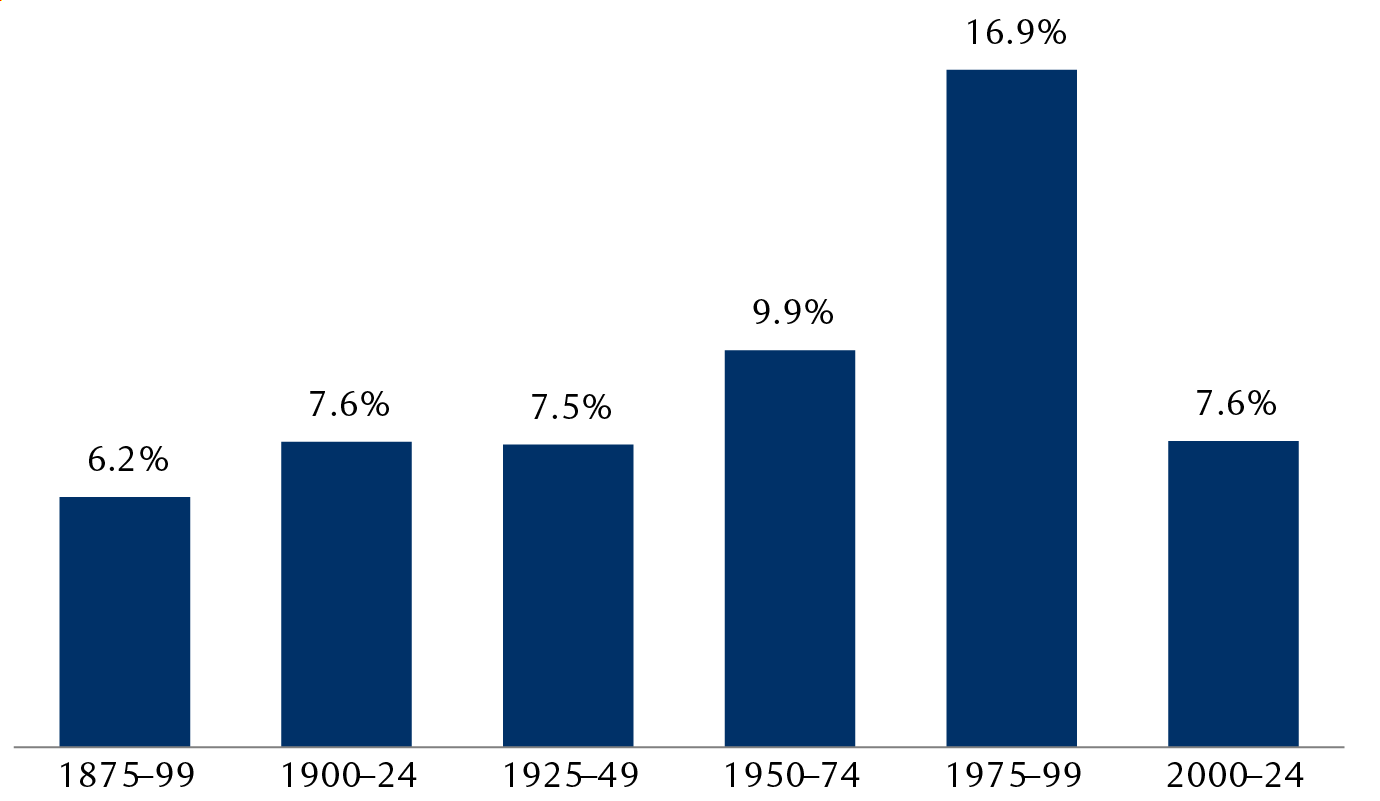

S&P 500 total annualized return

Total return estimated using price index levels from Bloomberg and Robert

J. Shiller’s data and dividend yield data from Bloomberg and Multpl.com.

Source – RBC Global Asset Management, Robert J. Shiller, Bloomberg,

Multpl.com

The column chart shows the total annualized return of the S&P 500 for

25-year periods. From 1875 through 1899 the return was 6.2%; from 1900

through 1924, 7.6%; from 1925 through 1949, 7.5%; from 1950 through 1974,

9.9%; from 1975 through 1999, 16.9%; from 2000 through 2024, 7.6%.

AI is also very important to U.S. GDP growth expectations because of the

dramatic size of big developers’ capital spending. Though AI capex will

continue to be sizeable, its growth will likely slow in 2026, and spending

could ultimately run into power-generation constraints.

Outside of the U.S., most developed economies are running stimulative monetary

and fiscal policies. Governments are increasing defence spending and central

banks are cutting interest rates. They are also faced with many similar

challenges, including anemic GDP growth, trade uncertainties, mounting fiscal

debt burdens and fraught politics.

The S&P 500 and large-cap indexes in Canada, Europe and Japan are all

trading at price-to-earnings multiples above their long-term averages.

Delivering above-average equity market gains from here would require an

unusual confluence of market-friendly economic, inflation and interest rate

conditions. Overall, the conditions necessary for global large-cap indexes to

deliver mid-single-digit returns plus dividends in 2026 are much less

demanding and more likely to occur.

Portfolios should be invested up to but not beyond a predetermined long-term

equity exposure with a plan for becoming more defensive if called for. We

would hold Market Weight positions in equities overall.

For more details on these views, please have a look at RBC’s Global Insight

2026 Outlook

on the web

or in

PDF format. PDF includes forecasts for commodities and currencies.

Regional perspectives

United States

For the equities bull market to persist, we think the economy and corporate

profits have to keep growing at healthy clips; the focus of the AI cycle needs

to shift to AI applications’ productivity and financial benefits accruing

outside of the tech sector; and the market turbulence that often accompanies

midterm election years will need to be avoided.

Overall S&P 500 profit growth will likely still be heavily impacted by the

technology sector given its large share of the market’s value. Questions about

an AI bubble will likely linger, but for now we see yellow warning signs

rather than a full-blown bubble.

The stock market’s elevated valuations, though a concern, may be sustainable

so long as economic and/or earnings growth do not buckle. We favour dividend

growth stocks and the Health Care sector.

Fixed income yields remain historically attractive, but we see scope for

modestly higher long-term yields, with core inflation likely to exceed 3.0

percent even as the unemployment rate is projected to rise modestly to

4.6 percent. This would put downward pressure on bond prices and, therefore,

total returns.

Credit markets remain historically rich, and we anticipate greater bond

supply, largely from tech firms, to weigh on overall performance.

Canada

The recent federal budget in which the government proposed CA$280 billion in

increased spending and capital investments over five years could provide a

further tailwind to the S&P/TSX. We continue to endorse businesses with

robust balance sheets, sustainable-to-growing earnings profiles, and proven

management teams with a track record of enduring market volatility.

Bank of Canada Governor Tiff Macklem has signalled that the central bank has

likely ended easing monetary policy for now. A steeper yield curve, as

long-term bond yields have edged higher on deficit concerns, argues for adding

duration in portfolios. Higher starting yields for long-term bonds help offset

the risk of further steepening.

United Kingdom

UK equities could continue to perform well as valuations are attractive. We

still favour the Financials sector, given the propensity for a high level of

shareholder returns. Should the Bank of England loosen monetary policy more

than markets currently expect, interest-rate-sensitive industries, such as

housing, could outperform.

With lowered fiscal risks following the recent tax-raising budget and looser

monetary policy, Gilts could potentially outperform, in our view. Treasury’s

bond issuance is likely past its peak and is being skewed away from long-dated

Gilts due to lower pension funds demand.

Europe

Economic growth should pick up somewhat in the region in 2026 thanks largely

to Germany’s increased infrastructure investment and defence spending. The

valuation of the STOXX Europe 600 ex UK Index—our preferred proxy for eurozone

equities—is slightly above its long-term average, which is warranted, in our

view, given the region’s improved medium-term growth outlook.

We continue to prefer sectors likely to benefit from fiscal stimulus, such as

select Industrials, Materials, and banks.

With increased overall bond supply and our expectation that yields will trend

higher in 2026, especially in Germany, we are cautious on European sovereign

bonds.

Asia-Pacific

The Chinese government continues to prioritize technology development, with a

focus on high-end manufacturing while domestic companies should continue to

benefit from the global AI spending boom, as they supply many key components.

The one-year trade truce reached between China and the U.S. should support the

Chinese economy and equity market sentiment in 2026.

Japan’s new prime minister has announced measures to counter inflation,

accelerated the timeline for defence spending increases, unveiled growth

strategies for cutting-edge industries and strengthened the U.S.-Japan

alliance. Overall, we view these measures as sufficient to help counter

inflation and boost sluggish middle-class consumption.

For more details on these views, please have a look at RBC’s Global Insight

2026 Outlook

on the web

or in

PDF format. PDF includes forecasts for commodities and currencies.

RBC Wealth Management is a business segment of Royal Bank of Canada. Please click the “Legal” link at the bottom of this page for further information on the entities that are member companies of RBC Wealth Management. The content in this publication is provided for general information only and is not intended to provide any advice or endorse/recommend the content contained in the publication.

® / ™ Trademark(s) of Royal Bank of Canada. Used under licence. © Royal Bank of Canada 2025. All rights reserved.

link